92% of millennial homebuyers say inflation has impacted their plans

Lifestylevisuals | E+ | Getty Images

It may come as no surprise that among millennials who have intended to buy a house this year, 92% said in a recent survey that inflation has impacted their goal.

Yet most of them aren’t letting it serve as a roadblock, according to the survey from Real Estate Witch, an education platform owned by real estate data firm Clever.

While 28% of those millennials are delaying their buying plans, the remainder say they’re responding by saving more money for the purchase (59%), spending more than expected (36%), buying a fixer-upper (26%) and buying a smaller home (25%).

More from Personal Finance:

Tax filing season is here. How to get a faster refund

Gen Xers carry the most credit card debt, study shows

Here’s what it takes to get a near-perfect credit score

Millennials — who are roughly ages 27 to 42 — are in their prime homebuying years. The typical first-time buyer was age 36 in 2022, up from age 33 in 2021, according to the National Association of Realtors.

Last year, first-time buyers made up 26% of home purchases, compared with 34% in 2021. The combination of year-over-year double-digit price jumps for much of 2022 and rising mortgage rates created an affordability problem for many buyers.

Home prices continue heading down from their highs

However, the situation is gradually improving as home prices continue sliding. The median price for an existing house was $366,900 in December, just 2.3% higher than a year earlier and down from $370,700 in November, according to the realtors association. Last June, the median price was $416,000 — 13.4% higher than in June 2021.

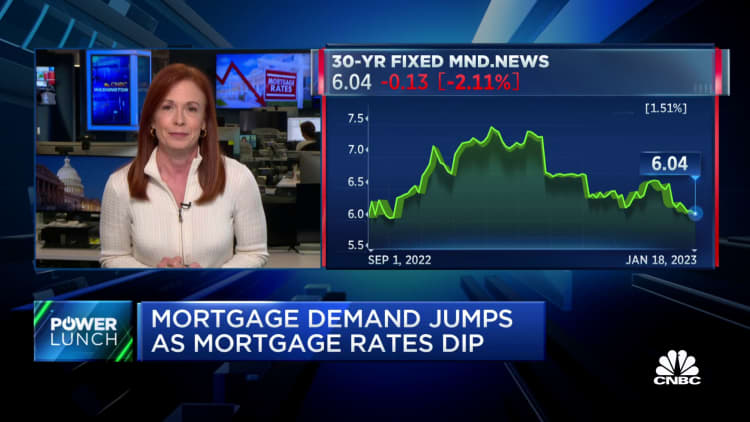

Additionally, interest rates on mortgages have eased. The average for a 30-year fixed-rate loan is 6.21% as of Jan. 24, according to Mortgage News Daily. That compares with 7.32% in late October. As buyers know, the higher the rate, the more their monthly payment is.

5% or 6% may be the ‘new normal’ for mortgage rates

While it’s impossible to predict where rates will be as the year progresses, experts say buyers shouldn’t wait around for mortgage rates to drop to where they were in 2020 and 2021 — below 3% or not much over it — because it’s unlikely to be seen again any time soon.

Rates were that low due to emergency actions taken by the Federal Reserve to prop up the economy in the wake of the pandemic hitting the U.S. in 2020.

“Those were unusual circumstances,” said Lawrence Yun, chief economist for the National Association of Realtors.

“Buyers should have the mindset that the new normal is a rate of 5% or 6%,” Yun said.

Houses are still selling quickly

One headwind that buyers may face is limited choices.

As of last month, there was a 2.9-month supply of homes — meaning at the current sales pace, that’s how long it would take to sell all listed houses if no more came on the market. That’s down from 3.3 months in November but up from 1.7 months in December 2021. A balanced market involves a supply of four to five months, according to Redfin.

“There’s not that much inventory in the marketplace,” Yun said.

“Even with the housing slowdown, days on the market are still less than a month,” he said. “That implies that people in the market to buy are finding a listing they want and snatching it up quickly.”

Homes that sit on the market longer may be a buying opportunity

If you’re hoping to find a seller who’s more likely to come down on price, one strategy is to look for homes that have been on the market longer.

“There’s usually a lot of competition for new listings,” he said. “If you find a home that’s been on the market for at least a month or two, it’s a great opportunity… sometimes sellers will take 10% to 15% off the list price.”

Additionally, be aware that while sellers had been less likely to go under contract with a contingency — i.e., making the final sale contingent upon, say, a home inspection — that dynamic has largely changed.

“Waiving the appraisal and waiving of inspections really walked hand in hand with low interest rates,” said Stephen Rinaldi, president and founder of Rinaldi Group, a mortgage broker based near Philadelphia.

Except for in premium areas, in most cases sellers are back to allowing contingencies.

Stephen Rinaldi

President and founder of Rinaldi Group

“Except for in premium areas, in most cases sellers are back to allowing contingencies,” Rinaldi said.

Also, if you’re looking at homes close to a city, it may be worth expanding your search radius, Yun said.

“There are always more affordable houses further out,” he said. “And those homes tend to stay on the market for a longer period.”

An adjustable rate mortgage may be an option

It may also be worth considering an adjustable rate mortgage if you’re trying to bring the cost down, Yun said.

With an ARM, the appeal is its lower initial rate compared with a traditional fixed rate mortgage. That rate is fixed for a set amount of time — say, seven years — and then it adjusts up, down or remains the same, depending on where interest rates are at the time.

“Usually the first home isn’t owned for a long period, usually it’s five or seven or 10 years,” Yun said. “So with that in mind, an ARM might make more sense because it offers a lower rate and by the time it’s set to adjust, it’s time to sell the house.”

While there’s a limit to how much the rate can change, experts recommend making sure you’d be able to afford the maximum rate if faced with it down the road.

You may be able to find an ARM whose introductory rate is at least a percentage point below fixed rates, Rinaldi said.

“I think it’s worth evaluating, depending on the person’s situation,” he said.